Von Julian callow, Head of European Economics, und Sreekala Kochugovindan, Vizepräsident, Global asset allocation Strategy bei Barclays capital

In the last two quarters of euorpäische economic engine has become noticeably slower. We expect gross domestic product in 2012 will drop slightly. In December, the European Central Bank has cut its intervention rate by 0.25 percent, and we expect 2012 other cuts.

The slow economic growth in the euro zone growth hides considerable differences among the member countries. We expect that Germany, Finland, Austria and other so-called 'core countries' growth in southern countries such as Italy, Spain, Greece and Portugal will surpass. The main reasons for this growth divergence are (a) differences in economic competitiveness (b) the level of indebtedness of the government and parts of the private sector, and (c) the different nature of financial market shocks. Given the high level of external debt held in Greece, Portugal and Spain, the continued prevalence of current account deficits in these countries is an indicator that further substantial adjustments must be made.

Between the core countries and southern countries have financing costs of the Government to high fluctuations. In Italy, for example, exceeded the two-year borrowing costs of the government in November 7 percent before falling to the current level of 6 percent. Comparable German rates hover around 0.3 percent. Consequently, companies will also be confronted in Italy and other southern countries compared to its German, Dutch and Austrian colleagues with significantly higher funding costs. Companies that predict future growth of its business sectors are likely to be more cautious with investments in southern Europe until the governments are able to show that they have control over fiscal policy and substantial liberalization measures.

The reasons for the weak growth in the euro zone and the divergence between countries are numerous and intertwined. Nonetheless, these are the currently most important underlying causes:

-

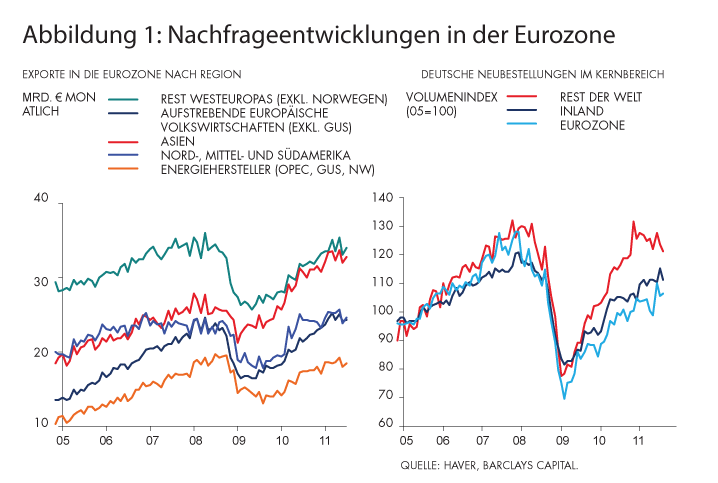

Foreign demand has waned in recent quarters: The drastic pressure by the rise in global inflation in the first half of 2011 undermined the real purchasing power of consumers. Furthermore, rising interest rates affected the global demand adversely, especially in most major emerging markets. This decrease in external demand was particularly among the leading exporters in the euro zone, such as Germany, considerable. It is, for example, in German orders very well documented (Abbildung 1).

-

During the summer and fall, it became apparent that Spain, Italy, Portugal, Greece and France had to announce additional austerity measures to meet the growing investor concerns about the sustainability of public finances. We estimate that this will reduce the real economic growth 2011/2012 by about one percentage point.

-

The intensification of the sovereign debt crisis in the fourth quarter of 2011, driven parts of the euro zone at the edge of a significant tightening of credit standards.

However, other regions, despite these adversities in the euro zone showed a stronger stabilization in the global context (such as the US and much of Asia).

Some of these effects, such as the reconstruction-related increase of activities in Japan, are temporary. Nevertheless, the reduction of global inflation is likely to have the effect that the demand growth can be stimulated and strengthened, while the central banks in emerging economies will be given at the same time a framework to ease policy (as a weakening of the reserve requirements for banks in China is visible ). The increase in retail sales in the US in recent months is a good example. Given the slight recovery in global demand growth, it seems likely that the euro zone could avoid a deep recession, when the problem of the financial sector contagion risk from Greece and Italy / Spain can be averted by taking decisive action.

We are still cautious regarding the European perspective, including Central and Eastern Europe (which is materially intertwined with the euro zone) remain. Investors and global companies should focus their attention on the faster-growing emerging markets with stable political conditions in Asia and Latin America. In the industrialized countries, investors in Canada, Australia / New Zealand and the Scandinavian countries are likely to focus on.